In a paper published by J.P. Morgan Asset Management titled “Housing: A time to buy”, the authors Dr. David Kelly and David Lebovitz make the case that the housing market is poised for a recovery.

It is well worthwhile to read and the graphs included paint a very dramatic picture of how things have changed over the past few years. Here are some of the main points made in the paper (my comments are in parenthesis):

Since 1959 the lowest annualized rate of housing starts recorded for any month was 798,000 and the average was more than 1.5 million units. Since January 2009, the average number of housing starts has been just 575,000 units. (We are now recovering from the early 2000’s building binge and the foreclosure aftermath. The current inventory is being slowly reduced and when it finally is down to normal levels new homes will have had to anticipate well or we will be left with a housing shortage. This is likely.)

From 2000 – 2009, the U.S. population grew by an average of 2.8 million people per year, with natural population growth contributing approximately 1.7 million people and immigration adding approximately 1.7 million people. On average 600 homes are started for every 1,000 person increase in the population. Given this ratio we should be seeing 1.4 million housing starts compared to the 572,000 that actually occurred.

From their peak in late 2005, nationwide median existing single-family home prices have fallen by 29% in nominal terms and by 37% relative to inflation. (Single family home prices have actually increased by 1.4%)

Since the first quarter of 2006, the value of home equity has fallen from $13.5 trillion to $6.2 trillion, a 54% decline.

Across a wide range of measures, the United States housing market is at its cheapest level in decades.

Housing prices as a percentage of personal income are about 27% below the average for the past 40 years. (Here we need to look toward the margins, not to the majority. It is the unemployed, underemployed and low net worth households who have been affected most during the housing bubble and those who most could use low interest rates cannot take advantage because of tight lending practices.)

Low interest rates have caused a 40 year low in mortgage payment as a % of personal income per household. 6.9% compared to the average of 14.4%. (Again, it is not average to have a mortgage payment only account for 6.9% of income.)

Since the late 1980’s monthly mortgage payments have averaged roughly 5% higher than renting the same home. From 2005 to 2007 the mortgage payment soared to nearly 50% more than comparable rent. It has now dropped and on average it is cheaper to buy than rent by 22%. (This does not hold true for most locations in Boulder County, see second point above)

Traditionally, houses have sold for 1.55 times the cost of building the home. The ratio peaked in 2005 when homes were selling at nearly 2 times the cost to build. The ratio is currently at 1.26. (Think of the premium above replacement cost as a combination of land cost and equity for resale properties and profit for new construction. Since 2005, both land costs and equity has dropped since 2005. In fact only for a new home developer can land cost be separated.)

All of the reasons suggest that housing should be ready for a quick recovery but alas there are other factors delaying the recovery.

High inventory of listed homes currently on the market. (Inventories in Boulder County are in check. As of October 31st inventories were down 13.7% from October 31, 2007)

High number of shadow inventory. Shadow inventory are homes in various stages of the foreclosure process which are yet to come on the open market. (Again, not a big problem in Boulder County)

In a recent poll, just 13% of Americans expected the price of their home to go up in the next year, and just 36% thought it would go up over the next five. A similar survey was done in 2006 and showed that 81% expected that the value of their homes would increase in the future. (Confidence in the market is a huge factor. Life changes happen despite the economy and life changes is what makes people want to move. There is pent up demand in the market just waiting for good news. Good news for most means that they can sell their home and feel good, not sell at a loss and lock in a great deal for 20 years. Too bad.)

The pieces of the puzzle are there and they point to a recovery. It is just taking longer than many of us had hoped. In the meantime take advantage of the anomalies in the market which are outlined above. Buying real estate is cheaper than renting and you can lock it in for 30 years.

There are many tactical ideas about real estate negotiation but in my opinion not enough is said about the emotional relationship between a buyer, a seller and an agent. Buyers and sellers don’t often meet in person. This can be a very good thing in many ways because the agents take the direct confrontation out of the process. But the downside of this lack of interaction is that buyers and sellers don’t get a chance to make a personal connection. They don’t get a chance to like each other. Their first interaction is the offer for purchase and this can be a very explosive introduction. “Hello Mr. Seller, nice to meet you. You don’t know me but I like your house but I think you are stupid to ask that much. I only think your house is worth $xxx. Oh, and by the way I want to keep your refrigerator, your window coverings and your grandma’s chandelier.” This usually doesn’t inspire an invitation to dinner.

Stephen Covey’s idea of an emotional bank account in “The 7 Habits of Highly Effective People” can be easily translated to the parties in a real estate transaction. Watch the video to see what a buyer, seller and agent can do to make friends with the other sides of the transaction. In doing so, negotiations will go much more smoothly and buyers and sellers won’t mind sitting together at the closing table (this by the way is getting less common).

Advice for Home Buyers:

Don’t make an unreasonably low offer.

Don’t ask for personal items which have been excluded from the sale.

Don’t be unreasonable and uncaring toward the seller.

Do write a personal letter so that the sellers can get to know you as a person (family).

Do compliment them on their home.

The goal is for the seller to want you to live in their home.

Advice for Home Sellers:

Have the house in tip top showing condition.

Fill out all disclosures accurately and thoroughly. Don’t try to gloss over the details. Giving more detail will earn the Buyers trust and respect.

Respond to offers quickly.

Keep the communication lines open.

Advice for Realtors:

Treat the other Realtor with respect, courtesy and go in with a win-win attitude.

Remember that you are not the one who is buying or selling. So don’t make decisions for your client. Lay out the options and let them decide.

Many times you will see “Home Warranty Included!” on a property listing. This sounds good right? But many times prospective buyers who negotiate for home warranties have the wrong idea about what a home warranty is and what it covers. Here are some answers.

A home warranty is basically a very limited insurance policy that covers certain home systems and appliances for a fixed time period. Usually when a home warranty is provided as a buyer incentive the warranty is good for one year after the closing. The cost of basic coverage is typically $275 – $400 and covers plumbing, heating, electrical, major appliances and water heater. There are limitations in coverage and plans do not cover preexisting conditions. Home warranties do not cover mold or structural damage.

Once the warranty is in place the new owner would call the warranty company first when an issue that requires a repair person to be called. The warranty company contracts with certain companies and sends them out to diagnose and fix the problem if it is determined to be covered. At the time of repair the owner pays a deductible. The owners share is usually around $50 to $60 per occurrence.

So is it worth it? Just like any insurance policy you need to weigh the probability of something happening and the severity of the cost if you didn’t have coverage with the cost of the coverage upfront. If someone else is paying it is definitely a good thing to have. If you are paying $400 year after year it may not pay off in the long run but it is an amount that is easy to budget and you won’t be surprised one year by needing a new furnace etc. The other consideration is the age of the home. If it is a newer home the chances of having a problem each year are relatively low. If you have an older home with older appliances the chances of needing repairs on a consistent basis increase.

Here are some home warranty providers in Colorado:

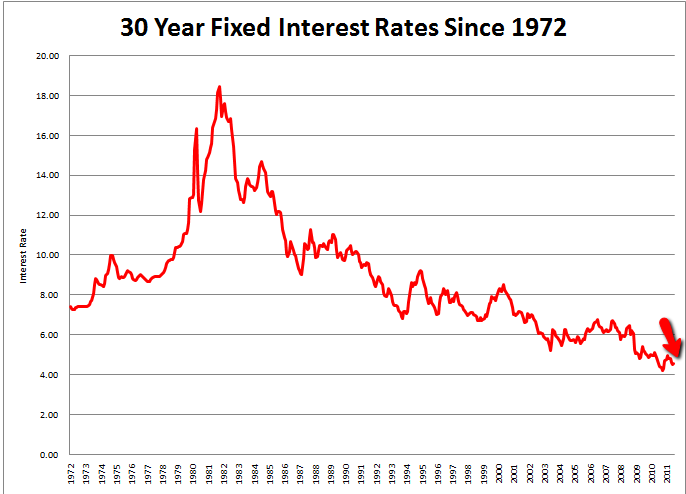

It seems like I have been saying this for years but now would be a fantastic time to buy a property. As interest rates drop the payment on the mortgage falls. What is surprising is how much. Say you have a $300,000 mortgage at 6% right now. 6% used to be a great rate. Anyway, right now for the same amount of monthly payment you can purchase a home with a $375,000 mortgage. That is $75,000 of free money! The effects can even be more dramatic if you have been in your home and have accumulated some equity. I am working with a buyer now who is purchasing a home $150,000 greater than their old home and their payment will be virtually the same. Did I say this is a great time to buy?

In order to sell a house in today’s real estate market a house must make a compelling case to the market. Some things like neighborhood and location within the neighborhood you can’t control. But set those aside and you are left with two key variables that are controllable and important to the sale.

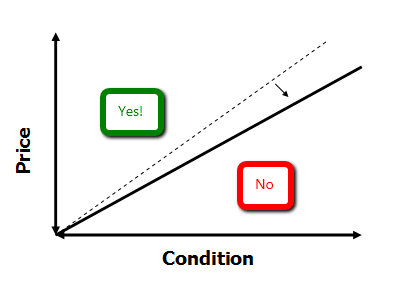

What I’d like to talk about today is being competitive in the market. The main variables a seller has control over is the price they ask for their home and condition and/or upgrades of the home. I have represented these two variables on an axis below so that I show you what I’m thinking. Basically, if your home is in great condition (and I mean exceptional) you can ask a high price compared to similar homes on the market. If your home is in poor shape you have to ask a lower price. This is not rocket science but it gets trickier when a house is somewhere between the extremes. It is in okay condition and has a middle of the road price. Looking at the chart below you can see the line running at 45 degrees. Think of this as the success line. Every house that fits above the line (price vs. condition) will most likely end up in a successful sale. Every home below the line will wallow until the price or the condition changes enough to get it above the line.

Right now the market is fairly slow. There are fewer buyers out there. This means that competition for sellers is tough. In order to be compelling to the small pool of buyers they have to bring a more compelling product to the market. This means that the line has shifted, sellers have to either improve their home to sell it for the same price or reduce their price to make it work.

Knowing where you are is the tricky part. I help my clients by giving good feedback and keeping them abreast of the market as it changes. The information you used to list your house is no longer valid. Get it priced right and have your house show the best it can. If you can’t afford to make improvements up front, lower your price. It’s simple economics.

A recent Wall Street Journal article reinforced some good points I have been trying to make about the viability of the housing market in the short and long term. The article which can be seen in its entirety here basically says that despite all of the negative news which surrounds the housing market, it is still a good idea to buy a home.

But the long-term benefits of homeownership remain very much intact. For now, at least, you can deduct the mortgage interest on your taxes—a big perk for people in higher tax brackets. You get to paint your walls any color you wish, without having to clear it with a landlord. And assuming you can buy a home for about the same price as you can rent one, buying will give you the ability one day to live rent-free. Come retirement time, a paid-off mortgage means your monthly expenses are significantly reduced, and you have a chunk of equity to play with.

So what might the next five years look like? Once the foreclosure mess begins to clear up, say housing economists, the traditional drivers of the housing market—demographics, affordability, loan availability, employment and psychology—should take over.

Demographics are going to play a key role in the recovery. According to the article, last year there were 950,000 new households formed and in the future that number will be more like 1.2 million per year. All of these new households need a place to live. Take that information and set it next to the fact that new building starts of residential units are at an all time low. You don’t have to be an economics PHD to figure out that when increasing demand and decreasing supply are mixed something has to give. What happens in real estate is that prices rise.

Another major premise of their article was that housing is becoming comparatively affordable. Prices dropping or remaining stagnant in a general inflationary environment make houses cheaper. On top of that mortgage rates are still amazingly cheap and won’t stay there forever. A quick side-note. I have clients looking to upgrade houses. The homes they are looking at are roughly $150,000 more expensive than the one they are selling. After running the numbers they figured out that their total payment was going to be about $160 more on a monthly basis. Peanuts!

Their last point was regarding the psychology of the consumer. Obviously, people have become very cautious and they are wondering if this is temporary or whether it is more of a permanent shift.

But it isn’t clear whether the fear will result in a prolonged change in attitudes, as during the Great Depression, or have little long-term impact, as was the case for the housing bust that shook California and the Northeast in the late 1980s and early 1990s. Eighty-seven percent of people surveyed by Fannie Mae said they preferred owning to renting, though access to schools, control over one’s environment and other quality-of-life issues now are seen as the key benefits of homeownership, with building wealth and other financial factors viewed as less important. In addition, 67% of renters surveyed by Zelman Associates said they planned to buy a home in the next five years.

I would recommend reading the entire article. I have only touched on the fringes.

make the case that the housing market is poised for a recovery.

make the case that the housing market is poised for a recovery.