If you have ever purchased a home with less than 20% down you have most likely heard the term “mortgage insurance”. Mortgage insurance is required to be purchased by the buyer when the equity is not sufficient to cover the risk. Different loan types require either an up-front payment or monthly payments. The mortgage insurance companies then insure the mortgage holders from some of their loss on that house in case of foreclosure, etc. Mortgage insurance companies only lose money when values drop and they are very careful (now more than ever) where they will insure properties and what they charge for their insurance.

Mortgage insurance companies are a great source for market information. They do research throughout the nation regarding the strength of local real estate markets. I thought it would be useful to see how a few companies see the Boulder and Denver markets. It is great information from companies who have much to lose if their risk projections are wrong.

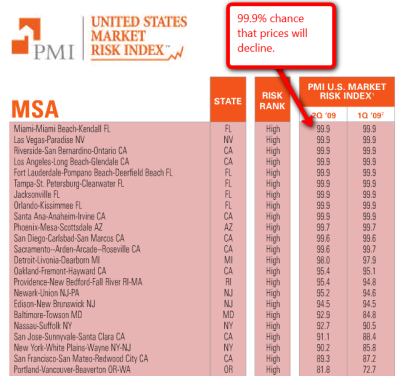

First let’s look at PMI. PMI uses a statistical model that assigns each Metropolitan Statistical Area (MSA) with a risk factor. This risk factor tells the percentage chance that the prices will fall over the next year. The chart below shows the highest risk areas. These markets show a 99.9% chance that prices will drop during the next year.

Boulder County has its own MSA and our prices have been pretty steady. Over the next year PMI says that there is only a 12% chance that prices will drop over the next year. This, for them Boulder is a low risk area.

Another company who does this type of analysis is MGIC.

MGIC ranks the largest MSA’s nationwide and gives a prediction on which direction the market is headed. They don’t rank Boulder, but they do rank Denver. Denver, which includes 11 metro counties, is listed as soft but “improving”. This is the only market in the country which is classified as an improving market. These third parties who are notoriously conservative see a brighter than average future for our area and this reinforces my optimism.

Tough market conditions call for creative ways to sell a property. More and more I’m hearing about an auction as a sales alternative. Buyers are looking for good deals through foreclosure and short sales but these are not always desirable homes. Auctions by privately owned homes tend to be a viable option for homes in the higher markets and so they tend to attract higher end buyers looking for a good deal. The marketing is slick, it looks like a good place to get a steal of a deal but WHAT IS THE CATCH?

There are many potential surprises when you attend an auction and they include?

Minimum prices that may or may not be stated clearly before hand. The words “minimum” and “reserve” can be used to make people think that they might just get the deal of the century when there is no chance that the seller is selling for less than X.

The owners and the auctioneers set the rules. If the rules change it is bad PR and will cause bad feelings but in the end what recourse does a potential buyer have if the seller reserves the right to cancel the auction at any time in the fine print.

Buying a house at auction may come with strings attached. Like, pay cash within 24 hours or use a certain lender.

Most auctions are final and binding so if you want to inspect the property do it before the auction.

Watch out for premiums. Auctioneers get paid a percentage of the sales price. Many times this is in addition to the sales price and paid by the buyer.

Watch out for bidders attached to the seller. The seller may advertise a no minimum, no reserve auction but have a bidder placed in the crowd who will bid the property up to at least the amount they want to sell for. If their placed bidder “wins” the bid the deal will mysteriously fall apart. We have had this happen recently in our market and the bids were inflated by a real buyer bidding against a relative. A week or so after the auction the real buyer was contacted by the seller asking if they still wanted to buy the property. The seller did not go through the registered agent who was helping the “real buyer”. Luckily the buyer smelled a rat and did not bite.

The best way to make money in real estate is to buy a property for the right price in the first place. No matter what you do to the property later, getting a good deal up-front makes all the difference. One of the best ways to get a good deal is to buy a foreclosure.

I bought my first place back in 1992 and it was a HUD foreclosure. I made a blind bid and won the auction by $500. I think the price was $65,000 and it was purchased with a minimum down FHA loan with my parents as co-signers. After living in it for 2 years, one with roommates and one with my newlywed bride, we turned it into a rental. After 8 years as a rental we sold it for $182,000 and bought two rental properties with the profit. Foreclosures combined with good market timing can provide a great springboard.

Over the last few years foreclosures have become a large part of the market in some areas. Historically, 5% of all outstanding mortgages are in some stages of delinquency. Currently that has doubled to 10%. Clearly, the combination of low equity loans, the abundance of secondary financing (HELOC’s), falling home prices (in some areas) and the recession have stirred up the perfect foreclosure storm.

They are out there, so how to buy them and profit from them? First off, buying a foreclosure is not for the faint of heart. In most cases these properties have been vacant for awhile and in many cases they were at best lived in very hard and at worst vandalized and stripped before the distressed owners left. You will not get a move-in ready house unless you are very lucky.

In my area, Boulder County and the surrounding suburbs, there has been a steady stream of foreclosures, but the vast majority have been in Longmont Colorado a town roughly 17 miles NE of Boulder. Longmont and Boulder have very different real estate markets. Boulder’s median price is somewhere near $550,000 and Longmonts is at $220,000.

If you are looking for a Longmont type deal within the city limits of Boulder, think again. There are very few foreclosures within Boulder and those that are out there sell at a discount when compared to the rest of the neighborhood, but finding a super screaming deal is very rare.

So how do you find a foreclosure? There are three types of foreclosures I will quickly highlight upon. First let’s look at the homes that are auctioned at the Boulder County Trustee’s Sale.

The homes at the trustees sale are fresh foreclosures. The owner’s have been given a chance to bring their loan up-to-date and keep their home but have not. The homes are then sold by a live auction process with the minimum bid provided by the current lender in advance of the sale. Bids must be a minimum of $1.00 over the lender’s bid. The successful bidder must provide certified funds for the exact amount of the winning bid by 1 pm the day of the sale. If you buy a home at the public trustees auction there is no inspection period or financing period. Have your cash ready. After the auction, the current lien holders have an opportunity to redeem the property and try to recover some of their losses. If no redemption attempts are made the sales is complete and the deed is issued 15 days after the sale. If a redemption is made the successful bidder will receive their funds back with interest. For more information about this type of sale in Boulder County and a list of properties for the upcoming auction go to Boulder Trustee Website.

In most cases banks end up owning the home after the public trustee auction. The homes then go through their REO (real estate owned) department and then re-sold through local Realtors. This process can take awhile but with patience they end up for sale on the MLS. These properties are identifiable as foreclosures by the ownership type and I can search for just REO homes. A buyer then negotiates with a representative at the bank. The properties can be financed and inspected, but all houses are transferred in as-is condition.

When a home with an FHA loan is foreclosed upon the U.S. Department of HUD takes the property and re-sells it via an online auction. These properties can be viewed in advance by contacting a HUD authorized broker (I have this certification). Bids are accepted online and you just have one chance to bid. The nice thing about HUD homes is that a buyer can get good FHA financing on the property with a minimum amount of down payment. Local information about HUD homes can be found at McBreo.com. If you would like help with a HUD home give me a call.

Now is a great time to buy. The interest rates are low (for now anyway), jobs are becoming more stable and there are some good deals out there. I’d love to help you make a good investment.

One of the greatest sources of letdown and conflict in a real estate transaction is the condition of the house after the Sellers move out. Provisions in the purchase contract allow for the buyer to do a walk through inspection prior to closing. I advise my buyers to do this walkthrough as late as possible so as to see the true condition of the property as it will be left. What to look for in a walkthrough could be its own topic but in summary; we are checking to make sure that the inspection items were completed as agreed upon, the inclusions are still at the house, that there has not been any recent damage to the house and finally to check the cleanliness of the house. The first three items are fairly “cut and dry”, either the refrigerator is in the kitchen or it’s not. I have found that cleanliness is very subjective. What may be very clean to one hurried, harried seller may be “filthy” to the buyer. I try to mitigate this by talking about this subjective divide as we write the agreement and make the language in the contract as plain and literal as possible. Instead of saying carpet cleaning (sellers picture the Bissell in their closet, buyers picture the $500 top of the line pro), I would make it clear that the carpets are to be cleaned by a professional with the receipt provided.

No matter what you try to plan for it is an issue. Sometimes it becomes an outlet for buyer frustration after a particularly tough set of negotiations. Sometimes it is a seller with good intentions but not enough time. Sometimes it is a professional hired who does a less than professional job. All I know is that I have hired cleaners, pitched in with the sellers as we did a last minute shine or have cleaned cupboards and closets myself. Small important details in making the closing day go smoothly and making my clients happy.

So some parting advice:

To Sellers:

Plan in advance. Closing and moving is a very hectic time and it is not always easy to complete all of those little last minute tasks.

Bring in help. Hire a cleaning company or better yet family. It is always very hard to go back to the old house to clean while all of your stuff is at the new house.

To Buyers:

Get it in writing. If you are worried about the condition of the house, set forth your expectations in writing.

Be realistic. Maybe you have to tidy up a bit when you move in to bring it up to “your” standards. Don’t let it ruin your day.

Purchasing a home is a huge undertaking and is most likely your largest investment. It is therefore wise to do everything in your power to minimize your risks. The first step is to hire a competent Realtor, that is where I come in. Your Realtor can then lead you through the process of intelligent due diligence. Some common items to consider: Is the asking price justified for comparable sales? How does the homes condition compare to others on the market? Are there any obvious flaws? What is the potential resale potential of the home? If the property is part of an HOA, can I live with the rules and the assessments? Can I live with the neighbors? etc…

Once these basic questions are answered a buyer usually then looks at the home more in depth. In our area a general home inspector is hired to look at plumbing, roof, electrical, appliances, foundation, drainage, furnace, etc. If there are any “red flags” he recommends that the buyer bring in a specialist to assess the situation and possibly bring in a bid. Another usual inspection in our area is a radon test. Usually the inspector administers the test for an added fee and provides the results of a 48 hour test.

Another inspection that is seldom used but very useful in older homes especially, is the video sewer line inspection. Some plumbers have a special camera that video tapes the sewer line as it exits the house, runs under the yard and enters the city line. The cost for the test runs around $300, but if it is an older home or one with a bunch of trees in the front yard, it can be well worth the cost. At the conclusion of the test the buyer ends up with a video of their sewer line with any breaks in the line marked in the yard. Costs to re-do a sewer line are usually above $4,000 so this is something that is best found out before closing.

The image above actually shows roots growing into a sewer line.

It’s easy to find homes on the internet. Search sites are everywhere but I know it is frustrating when the information is outdated. It also is a big job to sort through all of the homes each time to find the new listings or the price reductions. I can help! I can set up an automated search that sends new listings automatically to your email. This way you know what is happening in the market but don’t have to sort through all of the homes you have already seen or don’t care to view.

The best part is the website that goes along with the service. Each of my clients can have a personalized, pasword protected site in which to view all of the information available on a given home. On your MySite you can view, sort or delete listings so that you can easily come back and view or share what you have seen. The site updates automatically so when a house goes under contract or has a price change you will know about it when you log in.

This is a great service and I would like to set it up for you. I can set up searches for all of Northern Colorado. Take a look at the video above for a quck demo on how it works and how it looks. You will love it!