by neil kearney | Apr 2, 2009 | Boulder County Housing Trends, For Buyers, Real Estate 101 |

Interest rates are near historical lows and in many cases buyers are locking in rates that start with a 4. This is unheard of and represents one of the great buying opportunities in modern times. I just received a quote today for a 30 year conventional loan (below $417,000) with no discount points for 4.875%. This rate assumes at least a 10% down payment and a FICO score of at least 740.

I remember my first sale back in 1992, the interest rate was 8% and everyone at that time was saying that it was a pretty good rate, not the best, but reasonable. During the last decade we have become spoiled. Rates have been mostly in the 6 – 7% range with a few quick dips into the 5’s.

Now I hear people wondering if they should wait for rates to drop further, maybe to 4%. Hello, how much further do you want them to go? I guess it is human nature to get greedy when you start taking something for granted. But I say wake up and lock-in right now! 4.875% could turn into 6% in a flash and then where would you be? I have always been pretty conservative with my planning and when I am ready to purchase or refinance I plan using today’s rates and lock-in today’s rates. Call me crazy but I don’t think you should gamble on something that can change your payment every month by a significant amount. Here is a continuum of principle and interest payments at different interest rates. This assumes a $400,000 loan.

- 4.875% = $2,116.83

- 5% = $2,147.29 ($1 a day savings)

- 5.25% = $2,208.81 ($1,103 saved a year)

- 5.5% = $2,271.16 ($1,851.96 saved per year)

- 5.75% = $2,334.29 ($2,609.52 saved per year, a nice vacation?)

- 6% = $2,398.20 ($3,376.44 saved per year, that is $16,882 over 5 years and $101,293 over 30 years.

The point is, that interest rates are fantastic! If you are happy with your house, you should look into refinancing. If you might consider a move during the next few years, think about it now. That new house will never be more affordable. Good decisions now will pay off for years to come.

by neil kearney | Jan 27, 2009 | Boulder County Housing Trends |

Beyond sixth grade we don’t tend to think about tetherball much. It’s a pretty simple game. One of momentum, angles and coordination. Doug White a fellow broker here at Metro Brokers Boulder had a great idea about how tetherball is an analogy for the economy.

First, let’s review the basics. Tetherball is played by two people on opposite sides of a pole. From the top of the pole hangs a rope and at the end of the rope is a ball. The goal for each person is to push or hit the ball in a certain direction, either clockwise or counterclockwise around the pole. Before the rope begins to wrap around the pole the circumference of the arc is large and the ball seems to be moving relatively slowly. As the rope begins to wrap around the pole, the circumference becomes smaller and the time it takes for the ball to travel in a circle decreases. As the ball travels around the pole more quickly the players have less time to react. In the end the rope is fully wound around the pole and the ball hits the pole. The game is over and the ball begins to unwind. This is probably more than you ever wanted to remember about tetherball but here comes the analogy.

In our analogy the ball is the economy. On one side of the pole is “Positive Paul”. Paul stands for all of the positive forces of the economy. When Paul is doing well the economy is doing well. On the other side of the pole is “Negative Ned” and he represents all that would derail the economy. Since the early 1990’s Paul, for the most part, has been been doing well. All of the forces that make Paul work, like job growth, increased productivity, and population growth have been gaining momentum. As a result, momentum builds and companies are created, values on real estate and investments rise. With each arc around the pole momentum builds and the negative forces that slow the economy (Ned) has a harder and harder time even touching the ball. All is good.

During the last decade momentum has built up to a frenzied pace due to increased globalization, easy credit and unprecedented consumer confidence. As of two years ago, momentum had built up to a point where most thought it was unstoppable. The ball was whipping around the pole way out of the reach of Negative Ned. Positive Paul became complacent and cocky and then all of a sudden, just when Paul thought it would go on forever, Ned reached in and stopped the momentum. We are now seeing the excesses of the positive momentum resulting in the economy moving in the other way, quickly. The credit crisis, the housing crisis, unemployment, low consumer confidence; each of these factors is moving the ball in the negative direction. The negative momentum is moving fast since we still at the top of the pole. The economy seems to be unraveling.

Just as the exuberance (bad loans, over hiring, bad personal decisions) of the positive era caused the ultimate downfall of the economy. The correction (layoffs, record low housing starts, increased lending diligence etc.) is resulting in behaviors which will eventually turn it around.

What we need now are forces to stop the negative momentum. In a tetherball game more advanced players succeed because they know how to use angles. The strong hit is not nearly as effective if you hit it right to your opponent. To succeed a player must hit the ball so that the ball is at its highest point right where the opponent is. Right now, I think our overall financial re-trenching is weakening the negative forces, like a boxer punching the gut. What the government is trying to do with the proposed stimulus plan is to change the angle. To make the most of each action. Let’s hope they get it right.

by neil kearney | Oct 10, 2008 | Boulder County Housing Trends |

Here is What I Know:

Wow what a ride we have been in lately. It seems that people have been led to question the underlying value of everything financial. I try not to look at my retirement portfolio value and am constantly amazed by the huge

swings in the stock indices. With the realization that many companies have made huge bets on financial instruments that even they don’t understand makes one question what actually one owns. Is is the potential future profits or is it the hope that they didn’t make any really bad investments in other companies or contracts? The unknown brings fear and much of what we are seeing at this point is fear of the unknown. Banks and companies won’t lend to each other because they don’t know what skeletons they might have in their closet that would prevent a payback. With so many of the big names going down investors don’t know what is a good company and what is a bad company.

Real estate is certainly not immune from the unknown or from fear. How much value will I lose? Will I be able to sell my house? Will I be able to get a loan? Is this a bad time to sell? These are all questions that are on the mind of consumers right now. Here is what I know. The value of real estate can fall but it cannot disappear. You can use, live and enjoy a house. You cannot get any value out of a stock certificate.

When people talk about a return to quality, I keep thinking about my real estate investments. There may be a few fewer buyers out there right now but without exception everyone needs a place to live. The last few days people have been selling all of their investments and returning to cash (not a great move at this point, remember sell high – buy low). This does not hold true in real estate. Just because there is uncertainty does not mean that you should sell, you still need a place to live. The housing market is a semi-liquid investment, meaning that there are buyers,but it doesn’t happen right away. This illiquidity means overall stability. The national news made a big deal about a nationwide loss of 10% of home values, and this is not true in most areas. The Dow Jones average has lost 10% over the last few days, this is true instability.

All of thee news has scared people into believing that the sky has fallen. Obviously things have changed and we are in uncharted waters but people still need to move. People are still getting married, moving for jobs, getting divorced or having babies. Loans for most of those people (as long as they have a down payment and good credit) are still available. Sales of real estate are down but we are comparing today’s sales to those of the last few years which represented all time records.

Yes you need to be realistic. Yes you may need to be a bit patient but houses are still selling and people will continue to recognize real estate as a stable investment that provides a basic need.

Please call me if I can help you in any way.

Neil 303-413-6624

by neil kearney | Jan 22, 2008 | Boulder County Housing Trends, For Buyers, For Sellers |

Colorado Real Estate

Opportunity Knocks

Part 1: The Pond and the Lily Pad

Suppose you live in a large apartment building overlooking a 1.5 acre (65,536 sq. ft.) pond owned by the city. The city gardener wants to improve the looks of the pond and to improve the fish  habitat so he plants a 1 square foot patch of pond lily. Let’s assume that this is a very fast growing type of pond lily and that its area doubles every week. After the first week there are only two square feet of lily pads. Nothing really to notice. After 4 weeks there are 8 square feet of lily pads, still no one living in the apartment building would notice. After 8 weeks, the growth of lily pads is 256% but still even the most observant people would not recognize this as a trend. Only after 13 weeks when lily pads fill an eighth of the pond would the early trend spotters usually notice the difference in the landscape. Just two weeks after the early adopters see the lily pads growing the pond is half full. At this point, the media discovers the lily pad situation and reports the explosive growth. One week later the pond is full of lily pads. It took fifteen weeks of very slow deliberate growth to fill half of the pond and only one week to fill the other half. When would you notice the lily pads in the pond? Ask yourselves these questions: Are you too busy to look in the pond? Do you know enough about lily pads to understand what your looking for? Do you see the lily pads but don’t care until you hear about it in the news?

habitat so he plants a 1 square foot patch of pond lily. Let’s assume that this is a very fast growing type of pond lily and that its area doubles every week. After the first week there are only two square feet of lily pads. Nothing really to notice. After 4 weeks there are 8 square feet of lily pads, still no one living in the apartment building would notice. After 8 weeks, the growth of lily pads is 256% but still even the most observant people would not recognize this as a trend. Only after 13 weeks when lily pads fill an eighth of the pond would the early trend spotters usually notice the difference in the landscape. Just two weeks after the early adopters see the lily pads growing the pond is half full. At this point, the media discovers the lily pad situation and reports the explosive growth. One week later the pond is full of lily pads. It took fifteen weeks of very slow deliberate growth to fill half of the pond and only one week to fill the other half. When would you notice the lily pads in the pond? Ask yourselves these questions: Are you too busy to look in the pond? Do you know enough about lily pads to understand what your looking for? Do you see the lily pads but don’t care until you hear about it in the news?

Part 2: Tech Bust

Did you or someone you know buy a tech stock at the height of the boom? It was hard not get swept up in the fantastic media stories highlighting the huge IPO’s, the instant millionaires and the next big thing. Everywhere you went people were talking about how much money they have made by buying the stock of a company you had never heard with no sales and no product. The popular sentiment was “can’t lose”, “get in quick”, “if I could only get in on more IPO’s”, “nowhere but up”, “we are in a different era”… Obviously, this did not last and the lesson I took away from that era was that once ‘everyone” is talking about something, it is too late. In order to profit you must be a forward thinker, not influenced by the media. If you wait for the media to catch on, the trend is almost past and it is too late. The question is whether you are a forward thinker or a follower.

Part 3: Opportunity

Do you ever look back and wish you had bought real estate when it was more affordable, or just before the market took off in the 90’s, or before the rates went up. Now is the time to make up for those past mistakes. Now is a great time to buy real estate! Have you ever heard the phrase “buy when everyone else is selling”? These are the times when the smart money will be buying real estate. The national media has locked in to the housing story and will not let go. Locally, our paper is printing national stories with local bylines. People seem frozen by the negative news, waiting it out on the sidelines.

The CU Business Research Division in their recent 2008 Colorado Economic Forecast noted that “…the situation in this state is fundamentally different” (than the rest of the country). We did not participate in the recent excessive appreciation fueled by speculation that many other areas of the country had over the past four years. Our area is well ahead of the recovery curve. In my opinion our cycle is already in the process of turning. The news is gloom and doom but if you realize that real estate is local you can start separating truth from fiction. It is my hope to bring you that truth about our local market in this newsletter and it is my further goal to get you to see that the pond is just beginning to fill up with lily pads.

As always, we value your loyalty and friendship and I value your loyalty and friendship and am always available to answer any of your real estate questions. Neil Kearney 303-413-6624

by neil kearney | Jan 15, 2008 | Boulder County Housing Trends, For Sellers, Real Estate 101 |

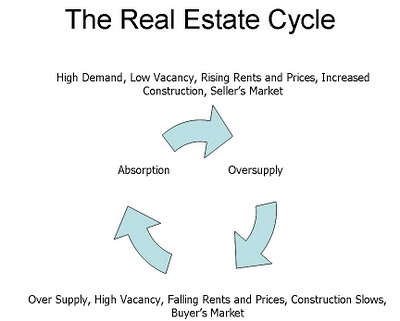

The Real Estate Cycle

I found this graphic on a power point slide I had put together a few years ago. Looking at it again, I firmly believe that we are in the “absorption” phase characterized by the arrow on the left side. Many of the symptoms of the bottom of the market have already happened and are improving. Rents have fallen but are now improving. Housing permits were down 26% last year. Vacancies have fallen, both in commercial and residential rentals.

I found this graphic on a power point slide I had put together a few years ago. Looking at it again, I firmly believe that we are in the “absorption” phase characterized by the arrow on the left side. Many of the symptoms of the bottom of the market have already happened and are improving. Rents have fallen but are now improving. Housing permits were down 26% last year. Vacancies have fallen, both in commercial and residential rentals.

It is still a buyers market and sales are not happening as quickly as some sellers would like but we are working again toward the top. Inventories are down and now is a great time to buy before prices spike again.

Have a great day!