by Neil Kearney | Feb 4, 2015 | For Sellers |

It used to be that to market a home meant putting a sign in the yard, copying a few brochures and placing the home in the local MLS service. Back in the day of MLS books, buyers and realtors had to wait a week for the book of listings to be updated. Now, the speed of information is almost instantaneous and it takes a diverse mix of marketing methods to attract buyers and maximize seller return. My goal is to maximize the appeal of my listings to prospective buyers through impeccable preparation, high quality deliverables and a beautiful Internet presence that gives each and every listing the custom feel that buyers appreciate. I fulfill this goal through the execution of my highly effective and proven marketing plan that puts the home, not the agency in the forefront.

The first step in my premier marketing plan is in detailed and early preparation. Your house deserves professional and experience representation and this begins long before the sign is placed in the yard. The first step in the preparation phase is to price the property correctly. Proper pricing results in maximizing the sales price for the Seller while still staying attractive to potential Buyers. Correct pricing takes into account comparable sales, the location, the condition of the property, the current market conditions and the competition. I take great care in analyzing and comparing your property to other homes with specialized spreadsheets I have developed over time that help us decide on the right price.

Once the price is set and the listing papers are signed, I go to work to maximize the appeal of the home by taking great photos and writing a compelling description. To many listings describe the property in terms of facts. I strive to describe the home as a lifestyle, a place to make memories, a place they want to live. The goal of the photos and remarks is to make the buyer want to look at the property in person. Almost all potential buyers are viewing listings online. Our first showing is online and the goal of my marketing is to make the buyer want to see the property in person.

After the photos are done and the description is written, my hub and spoke marketing plan is implemented. The hub is a custom website that I build from scratch. This is a true custom website developed from scratch and with it’s own website address. On this website I can tell the full story of your home, display all of the photos, describe the location, the neighborhood, display links to the HOA, show the brochure and the MLS sheet, etc. When a buyer wants more information we want more than 500 characters (the limit on MLS and other online sites) to tell the full story of why this home is different and why they should see it. The custom website is where interested buyers go to get the information they want and it’s where they send their family to share their excitement. This is where we point all of our other marketing. This is where we can give a full and controlled experience to our potential buyers.

The spokes of my premier marketing plan includes print, online and Realtor-to-Realtor advertising. The diagram on this page shows how I use a broad spectrum of marketing methods to reach potential buyers. All of my marketing is done with a feel of substance and quality.

Print marketing includes a sign, custom brochures, a sign rider with the website address and consistent display advertising in the Daily Camera.

Our strategic online marketing includes websites across all sectors. These include national websites such as Realtor.com and Redfin.com. Regional websites such as Coloproperty.com. Local websites such as AtHomeColorado.com. Competitor websites such as Remax.com, COHomefinder.com, and wkre.com. Of course your property will be featured on the KearneyRealty.com and NeilKearney.com websites as well. The goal of online marketing is to impel the buyer to take the next step.

Our marketing to other Realtors includes a thorough MLS listing, which includes the compelling description and beautiful photos and email marketing to our local list of over 800 agents. With the MLS listing, it’s important to have done all of the prep work upfront because you only have one chance to make a good first impression. I have established a reputation among my peers based on impeccable ethics and easy communication. Other agents like working with me and they know when they bring an offer it will be handled promptly and with complete integrity.

by Neil Kearney | Feb 2, 2015 | For Buyers, For Sellers |

I just received this letter of recommendation from a recent client. I loved working with them and I’m so happy that they appreciated my efforts and the results. The website for their home that I built is located at www.SunriseRanchHome.com

“Though we find it hard to express how much we appreciate and value Neil Kearney’s professional, ethical, kind and extremely effective representation of our home, it was not difficult for Neil to describe and represent our home in a way that was extraordinary.

From the moment we met Neil, we knew we had found the realtor who was looking out for our interests and advocating a sales plan that would ensure the most for our investment. Neil took extraordinary, professional photographs of our home, and his images and words in a beautiful brochure and amazing website created for our home reflected his passion for his job and for representing his clients in a way that is unsurpassed.

You could not hope to find a more experienced, more professional realtor to get the absolute best value out of your property – but the bonus is that you will undoubtedly find a friend. Our sale and purchase experience were benefited by his calm good humor and his expert eye – pointing out the problematic stucco, or the vacant lot across the street zoned for commercial development. Neil is extraordinary at his profession – skilled, calm and phenomenal – our recommendation is without reservation, and WITH great enthusiasm.”

Brad and Cindy Taylor

Former Director of Consumer Protection for the Boulder County D.A.’s office

I always have the capacity to work with new clients, so if you are looking for the type of service that is described in the letter above please contact me to get started. 303-818-4055 cell or Neil@KearneyRealty.com

by Neil Kearney | Dec 18, 2014 | For Buyers, General Real Estate Advice, Real Estate 101 |

Here are some of the reasons why people buy their first home.

Here are some of the reasons why people buy their first home.

- Tired of paying rent / rents are rising.

- Home prices are rising and if they don’t buy now they might be priced out of the market.

- Just got married.

- Just got a great new job.

- All my friends are buying a place and it seems like a good idea.

All of these reasons are reasonable, but none of them hit on the key factors that a first time home buyer should consider when they are thinking about buying a home. They can push you in the right direction but they don’t ensure an intelligent purchase.

Buying a home is one of the best ideas you can make. It is a great long term investment, your payments are tax advantaged, with each payment you are gaining equity and you get to live in a place you can make your own. It’s a win, win, win! However, the keys to making it a good investment have much to do with your stability and your budget.

I mentioned in the previous paragraph that owning real estate was a great long term investment. Unless the market is appreciating very quickly you will be doing very well to break even if you need to sell within two years. Real estate is cyclical so not everyone gets lucky and makes the purchase right before prices take off. In many markets prices are just now getting back up to 2007 levels after a big decline. If you bought in 2006 and needed to sell in 2010 you lost money. So the first question to ask yourself when you are considering a home is: “How long will I be living in this house?” If you answer is less than five years it might be better to rent. A key to making real estate an investment, not just a place to live is the ability to wait out market cycles.

Besides geographic stability the other main thing to consider is affordability. The first step to figure out what is affordable is to take an in depth look at your finances. Examine your long term financial goals such as savings, retirement, kids college, vacations, etc., and figure out how to make it all fit within your budget. When you know your comfort level regarding monthly payment call a mortgage lender to get pre-approved. Most likely you will be approved for more than what you are comfortable paying. If you over-extend yourself with your new house you will feel burdened instead of smart. Pick a payment that is comfortable for you and that allows you to keep your savings and lifestyle goals in tact.

Some practical considerations regarding affordability:

- Plan ahead for future changes in income. Do you plan to become a one income family after you start a family? Don’t lock yourself into a payment that requires two incomes.

- Have you saved enough of a down payment? Low down payment options are available but they require an additional payment called mortgage insurance. If you have less than 20% down it might be a good long term decision to delay the purchase and save every penny you can until you have what you need.

- As interest rates rise your payment dollar buys you less house. If you are almost ready to buy and your qualification is right on the edge it might be good to lock in a home before interest rates rise. To read more about how much this can affect your payment see my article The Impact of Interest Rates on Home Affordability.

- Credit scores have a huge impact on your ability to buy a house. If you have a credit score of less than 760 your qualification or the interest rate you are offered will be negatively affected. To check your credit score for free (with no strings attached) go to www.AnnualCreditReport.com. If you find out that your credit score will negatively impact you, figure out why your have a low score and start fixing your FICO score.

by Neil Kearney | Dec 8, 2014 | General Real Estate Advice, Real Estate 101 |

In Colorado, when there is more than one buyer or entity purchasing real property, the buyer(s) can specify how they will hold title. On the Colorado approved “Contract to Buy and Sell Real Estate” in section 2.1 buyers have the option to take “title to the Property described below as Joint Tenants, Tenants in Common or Other. Below I will spell out the main differences between joint tenants and tenants in common.

Joint Tenants

Joint tenancy is characterized by right of survivorship. When a property is owned by joint tenants, and one of the owners dies, the interest of the deceased owner automatically gets transferred to the remaining surviving owners. For example, if five joint tenants own a house together and one of them dies, each of the four remaining joint tenants ends up with 1/4 share of the property. Regardless of what the deceased owners will says. In 2008 the laws were changed to allow for unequal interests in the property by the owners. For example, instead of an elderly parent owning a 1/2 share along with their child to whom they would like to leave the house, the ownership could be split 99% / 1%. When the parent dies the child would then own 100% interest in the property.

Joint tenancy is most often used by married couples or multi-generational families who own real estate together.

Tenants in Common

There are three main differentiating characteristics of tenants in common ownership. The first is, like joint tenancy the ownership interest can be split up into different percentages. For example Owner A can own 60%, Owner B 15% and Owner C 15%. The second feature is that the mix of owners and the percentage of ownership can be changed at any time. Owners can be added or subtracted at any time by mutual execution of legal documents. Tenants in common doesn’t have rights of survivorship. If in our example Owner A dies, his 60% interest would go to his estate unless his will specifies that his interest shall be split between the remaining parties.

Tenants in common is most often used by unrelated parties such as friends, un-married couples, business partners or family members where one person is putting down more assets than the other.

This article isn’t intended to give legal advice. Please seek professional guidance when making legal decisions.

by Neil Kearney | Dec 4, 2014 | For Buyers, Real Estate 101, Statistics |

Most real estate buyers can’t afford their home. A first time buyer who saves up for a down payment, has good credit still can’t afford their home. Being able to afford their home means paying cash. When a buyer says that they can afford a $300,000 home for example what they actually mean is that their budget allows for them to afford the payment on the mortgage that goes along with a purchase price of $300,000.

Most real estate buyers can’t afford their home. A first time buyer who saves up for a down payment, has good credit still can’t afford their home. Being able to afford their home means paying cash. When a buyer says that they can afford a $300,000 home for example what they actually mean is that their budget allows for them to afford the payment on the mortgage that goes along with a purchase price of $300,000.

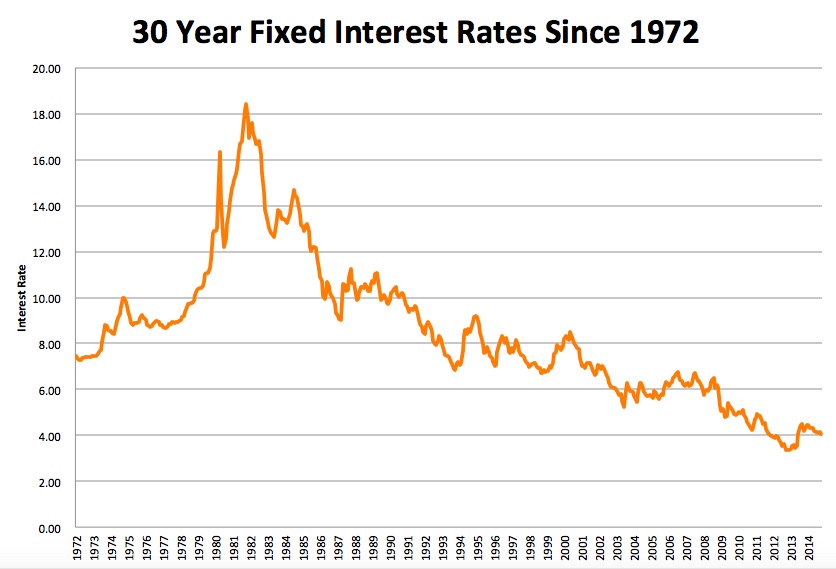

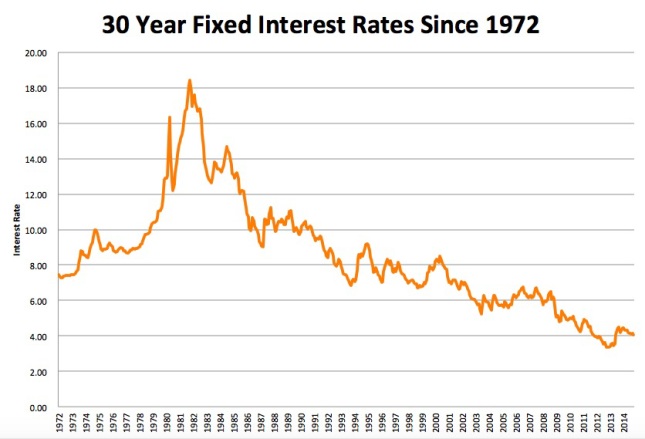

When a buyer is in the market for a home, the search process is usually short enough so that the mortgage interest rates are relatively stable. But this is not always the case. For a long time now, interest rates have been historically low but as you can see from the attached graph they are still historically VERY LOW. At a recent meeting I attended, the Chief Economist of the National Association of Realtors predicted that interest rates would rise .5% by spring and be up near 6% by the end of 2016. These are big jumps in a market where we have gotten very used to low rates. I fear that many potential buyers are beginning to expect the rates to stay where they are. And I hate to be the bearer of bad tidings, change is the only constant and the cycle for increasing interest rates is coming. When I broke into the real estate business as a green agent in Boulder Colorado in 1992 8% was a great rate. Now 4% is considered a great rate.

So when interest rates do go up the issue will not be how expensive a house you can afford, it will be how big a payment a buyer can afford. So, let’s look at how sensitive a payment is to changes in interest rates. This is called payment elasticity. Let’s consider the following scenario.

- A buyer has been pre-qualified for a mortgage payment (not including taxes or insurance) of $1800 per month. Let’s assume a current interest rate of 4.5%, at this rate they qualify for a top home price of $355,000.

- They are excited about their home search and on their first time out with their Realtor (hopefully me :)) they see some really great homes. They are happy with the type of home they can get, but decide to keep looking.

- They have a trip planned and then people coming into town, so they are not able to look at homes for a number of weeks. After that they find that there isn’t much to look at. The time between first looking at homes and their second viewing trip is two months. During that time interest rates increase from 4.5% to 5%. The next time out they find a house listed for $355,000 and write an offer for $350,000. The offer gets accepted and everyone is really excited until they talk to their lender who informs them that “interest rates have increased and they can no longer qualify for the house they have a contract on. Their top price range is now $335,000”. Crushed! Disappointed! Upset! Betrayed! These are just a few words that come to their minds as they quickly cancel the contract.

It’s called interest rate risk and it can really happen. In my scenario, the buyers lost $20,000 of purchasing power in a short amount of time as interest rates climbed just 1/2%. To see how this looks with real payments take a look at the chart below. In this scenario for every 1% increase in interest rates they lose $40,000 of purchasing power. If in our scenario the buyers find a way to qualify their payment just went up $106 per month or

Moral of the story – Don’t ignore interest rates. If you are happy with your payment and happy with a house, jump on it. This could become an issue in the near future.

Moral of the story – Don’t ignore interest rates. If you are happy with your payment and happy with a house, jump on it. This could become an issue in the near future.

My source for the historical interest rates is FeddieMac